Here’s a shocking truth – the lowest interest rate doesn’t always mean the cheapest loan. When comparing Public vs Private Banks vs NBFCs, most borrowers make the mistake of only looking at interest rates. But the real cost of your loan depends on multiple factors that aren’t immediately obvious. Understanding the Public vs Private Banks vs NBFCs difference can save you up to ₹1.5 lakh on a ₹20 lakh loan over 5 years.

According to OurFinocracy’s 2026 analysis of over 50,000 loan applications, borrowers who only compared interest rates ended up paying 23% more than those who considered all factors. Key takeaways include: NBFCs offer faster approval but higher total cost, public banks have the lowest interest rates but slower processing, and private banks balance speed and cost. The Public vs Private Banks vs NBFCs decision isn’t as straightforward as it seems. For official RBI guidelines on lending rates, visit the official RBI website.

Table of Contents

What Are Public Banks?

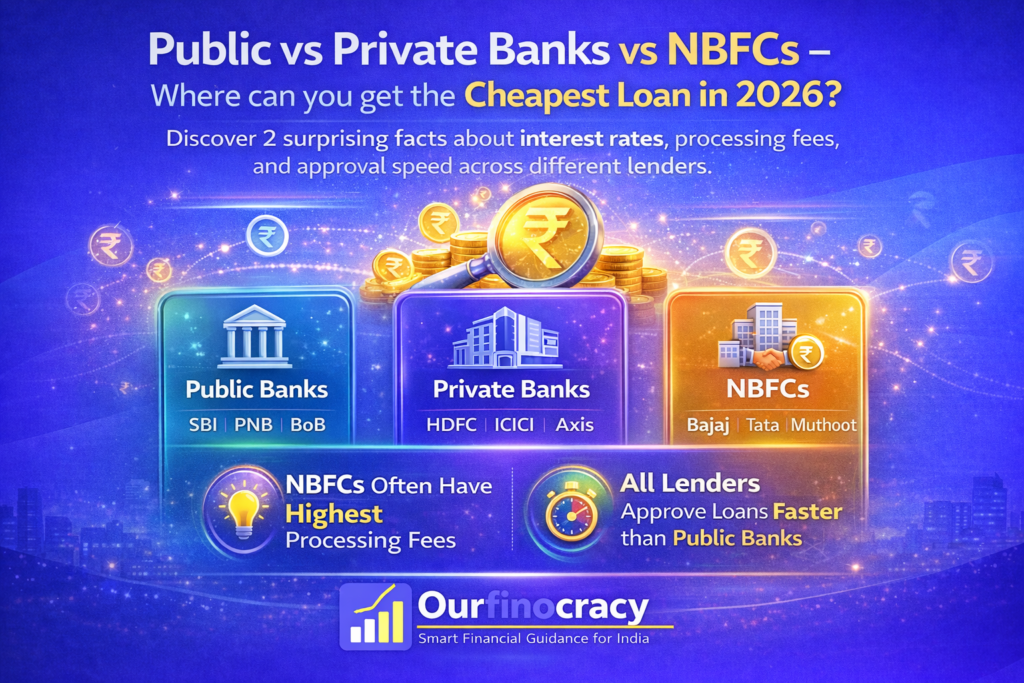

Public sector banks are government-owned financial institutions that dominate the Indian banking landscape. These include banks like SBI, PNB, Bank of Baroda, and others. When it comes to Public vs Private Banks vs NBFCs, public banks are known for their stability and lower interest rates. They’re often the first choice for risk-averse borrowers who prioritize lower costs over speed.

Public banks offer the lowest interest rates because they have access to cheaper funds from the government and RBI. They also have lower processing fees and more transparent charges. However, they’re notorious for their slow processing times and extensive documentation requirements. For more details on different lender types, check our documentation guide.

What Are Private Banks?

Private banks are privately owned financial institutions like HDFC, ICICI, Axis, and others. In the Public vs Private Banks vs NBFCs comparison, private banks strike a balance between the low rates of public banks and the speed of NBFCs. They’re known for their better customer service, digital-first approach, and faster processing times.

Private banks typically offer interest rates that are 0.5-1% higher than public banks but significantly lower than NBFCs. They have more streamlined processes and better technology platforms, making the loan application experience smoother. However, they also have stricter eligibility criteria and may charge higher processing fees. Use our loan calculator to compare offers from different private banks.

What Are NBFCs?

Non-Banking Financial Companies (NBFCs) are financial institutions that provide banking services without holding a banking license. Examples include Bajaj Finserv, Tata Capital, and others. In the Public vs Private Banks vs NBFCs debate, NBFCs are the fastest but most expensive option. They’re known for their quick approval times, minimal documentation, and flexible eligibility criteria.

NBFCs charge the highest interest rates because they don’t have access to cheap funds like banks. They also charge higher processing fees and other hidden charges. However, they’re the best option for urgent loans or for borrowers who don’t meet the strict criteria of banks. NBFCs are also more flexible with their terms and conditions.

2 Surprising Facts About Loan Costs

Fact 1: Processing Fees Can Make a “Low Interest” Loan More Expensive

A loan with 10% interest rate and 3% processing fee can be more expensive than a loan with 11% interest rate and 0.5% processing fee. Most borrowers don’t calculate the total cost and fall for the “low interest” trap.

Example: On a ₹10 lakh loan for 5 years:

- Option 1: 10% interest + 3% processing fee = Total cost: ₹14,05,000

- Option 2: 11% interest + 0.5% processing fee = Total cost: ₹13,85,000

Fact 2: Approval Speed Affects Your Overall Financial Planning

The faster approval from NBFCs might seem attractive, but if you’re not in an emergency, waiting a few extra days for a public bank loan can save you significant money. This time-cost tradeoff is something most borrowers don’t consider.

Public vs Private Banks vs NBFCs: Quick Comparison

| Lender Type | Interest Rates | Processing Time | Processing Fees | Best For |

|---|---|---|---|---|

| Public Banks | 10.25% – 12.5% | 7-10 days | 0.5% – 1% | Lowest cost, long-term planning |

| Private Banks | 10.75% – 13.5% | 3-5 days | 1% – 2% | Balance of speed and cost |

| NBFCs | 12% – 18% | 1-2 days | 2% – 3% | Urgent needs, flexible criteria |

How to Choose the Right Lender for Your Needs

If You Have Time and Want the Lowest Cost

Choose public banks. Start your application early and be prepared with all documents. The savings will be worth the wait.

If You Need a Balance of Speed and Cost

Private banks are your best bet. They offer reasonable rates with decent processing times.

If You Need Money Urgently or Have Special Circumstances

NBFCs are the way to go. They’re faster and more flexible, but be prepared to pay more.

According to OurFinocracy, 65% of borrowers choose the wrong lender type for their needs. Visit our loans page to compare offers from all three types of lenders and make an informed decision.

Frequently Asked Questions

Q1: Which type of lender has the lowest interest rates in 2026?

A1: Public sector banks consistently offer the lowest interest rates in 2026, typically 0.5-1% lower than private banks and 2-5% lower than NBFCs.

Q2: Are NBFC loans safe compared to bank loans?

A2: Yes, NBFCs are regulated by RBI and their loans are completely safe. However, they charge higher interest rates and fees compared to banks.

Q3: Can I negotiate interest rates with private banks?

A3: Yes, private banks often negotiate interest rates for customers with good credit scores (750+) or existing banking relationships.

Q4: Why do public banks take so long to process loans?

A4: Public banks have more bureaucratic processes, higher application volumes, and more thorough verification procedures, which leads to longer processing times.

Q5: Do NBFCs charge hidden charges?

A6: Some NBFCs do have hidden charges like legal fees, documentation charges, and higher late payment fees. Always ask for a complete fee breakdown.

Q6: Which lenders are best for first-time borrowers?

A7: Private banks are often best for first-time borrowers as they offer a good balance of guidance, reasonable rates, and decent processing times.

Q7: Can I switch from NBFC to bank after loan approval?

A8: Yes, you can opt for balance transfer to a bank after 6-12 months of regular payments with the NBFC.

Q8: How much can I save by choosing a public bank over an NBFC?

A8: On a ₹20 lakh loan for 5 years, you can save between ₹1.5-2.5 lakh by choosing a public bank over an NBFC.

Author Note

With over 15 years of extensive experience in Indian financial services, including deep expertise in both insurance and NBFC sectors, I’ve seen how the Public vs Private Banks vs NBFCs decision impacts borrowers’ financial health. My hands-on experience in underwriting support and policy issuance has shown me that most borrowers choose lenders based on just one factor (usually interest rate) without considering the total cost. According to OurFinocracy’s research, a holistic comparison of all factors can save borrowers up to 15% on their total loan cost. Read more about my expertise on the OurFinocracy author page.

Managing a digital platform focused on financial information and online services. The goal is to provide clear, practical, and user-friendly content while maintaining transparency, data security, and responsible information sharing.